Gratuity

Pension

Defined benefit scheme

Defined contribution scheme

Savings and investments

Gratuity - prior to the Pension Reform Act many organization ran a ‘’Gratuity Scheme’’ which was similar to the Contribution Pension Scheme.

With the advent of the Pension Reforms, most companies have cancelled their Gratuity schemes.

PENSION FUND MANAGEMENT

Pension funds are managed to provide post retirement benefits to employees.

A pension plan is a retirement plan that requires an employer to make contributions into a pool of funds set aside for a worker's future benefit. The pool of funds is invested on the employees’ behalf, and the earnings on the investments generate income to the worker upon retirement.

Some of the bodies involved in the management of Pension Funds are;

National Pension Commission (PENCOM)- which regulates and supervises pension matters

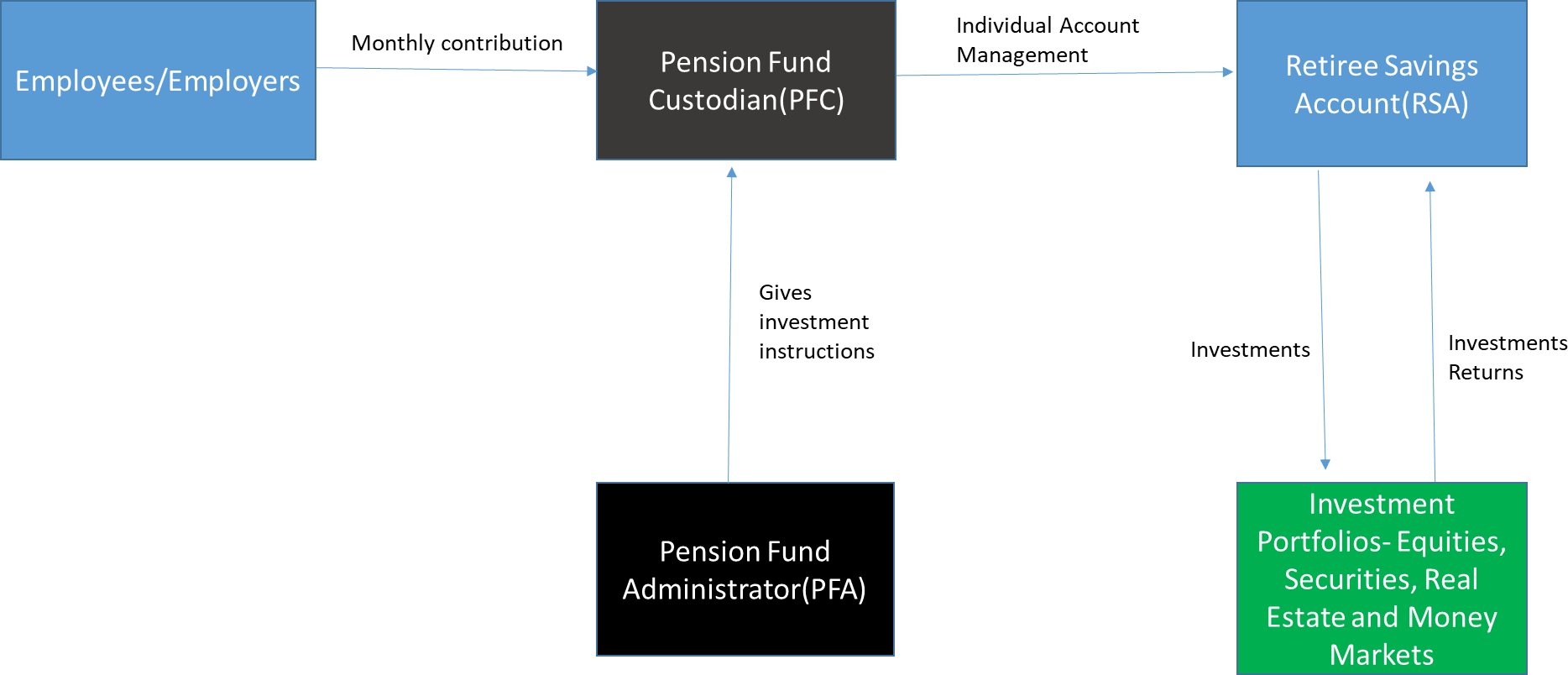

Pension Fund Administrators (PFAs) They are Private Limited Liability Companies licensed to manage pension funds under the Pension Act2004.

Pension Fund Custodians (PFCs) They are banks licensed to hold the pension fund assets on behalf of the PFA

PENSION AS A MAJOR SOURCE OD INCOME

A pension is a fund into which a sum of money is added during an employee’s employment years, and from which payments are drawn to support his or her retirement from work in the form of periodic payments.

The major source of income for most retirees is public and private pension.

Having a pension plan is one of the most secure insurance policies for your future upon retirement, and it is important that when you are about to start a new job, you ensure that a pension plan is part of your package.

So, you might ask, what happens to your pension contributions when they are deducted? Do they just sit in the account until you retire and can withdraw them? The answer is no, the Pension Fund Administrator gives investment instructions to the Pension Fund Custodians on how to invest them in certain approved categories of investments e.g. government bonds, Treasury bills, Real estate, money markets and other securities as well as shares of public limited companies. This is strictly monitored by the Pension Fund Commission, with substantial fines and penalties for non compliance.

ASSESSING FUNDING AT RETIREMENT

The process of documentation actually starts six months before you retire. For FG employees, they have to go for the Bond verification exercise organized by PENCOM. Basically, this exercise is to enable PENCOM to consolidate their account and ensure their accrued rights are paid immediately once they retire. For Private sector employees, your PFA has to confirm that all contributions due to you have been made. This process is called ‘consolidation of account’. After this is done, the process of actual payment should take about 3weeks.

Accessing Funding at Retirement having attained the age of 50 years:

A holder of a retirement savings account shall, upon retirement or attaining the age of 50 years, whichever is later, utilize the amount credited to his retirement savings for any of the below benefits

Withdrawal of a lump sum provided that the amount left after the withdrawal shall be sufficient to procure a programmed fund withdrawal or annuity for life

Programmed monthly or quarterly withdrawals calculated on the basis of life expectancy

Accessing Funding before 50 years of age following voluntary retirement or redundancy:

A holder may be allowed access to 25% of the Retirement Savings Account if he/she voluntarily retires, disengages or is disengaged from employment on the advise of a suitably qualified physician on account of mental or physical health, disability or at the age of 50 years in accordance of the terms of employment. This is on the condition that the withdrawal shall only be made after four months of such retirement and the employee does not secure another employment.

ILLUSTRATION

Mr A retiring at Age 42, can withdraw 25% 0f his RSA after 4 months if he does not secure another employment

Mr B retiring at the age of 50, can withdraw a lump sum of 50% of his RSA if the amount is higher than half of his annual salary as at the time of retirement

ASSESSING FUNDING AT RETIREMENT cont.

Where an employee dies, his entitlements under the life insurance policy shall be paid by an underwriter to the named beneficiary.

Upon receipt of a valid will admitted to Probate or Letter of Administration confirming the beneficiaries under the estate of the deceased employee, the Pension Fund Administrator shall, with the approval of the Commission , release the amount standing in the retirement savings account of the deceased to the personal representative of the deceased or to any other person as may be directed by a court of competent jurisdiction in accordance with the terms of the will or the personal law of the deceased employee , as the case maybe.

HOW YOUR PENSION CONTRIBUTION FLOWS

PENCOM new guidelines on voluntary pension contributions

A circular dated 16 November 2017 has been issued by the National Pension Commission (PENCOM) to all licensed Pension Fund Administrators and Custodians. Below are the highlights:

In respect of voluntary contributions (VCs) by Mandatory Contributors:

Withdrawals from VC account is limited to once every 2years

Taxes will be deducted on any income earned if withdrawn within 5years

Total withdrawal from VC account is limited to 50% while the balance of 50% must be kept to augment contributor's retirement benefit

In respect of VC by Exempt Contributors (including foreigners)

Withdrawals from VC account is limited to once every 2years

All the VCs may be withdrawn after 2 years but subject to tax on both the principal contribution and income earned thereon

Withdrawals made after 5 years from date of contribution will be fully tax exempt

RETIREMENT SAVINGS PLANNING

The share of each section of the pie that would consume your retirement income will depend on your age at retirement.

Planning now is crucial in order to provide time to determine your financial goals as well as decide how you really want to spend your time.

VARIABLE EXPENSES – TRAVEL, LEISURE ACTIVITIES, GIFTS,ETC.

FIXED EXPENSES – MORTGAGE, UTILITIES, INSURANCE, MONTHLY HEALTHCARE AND PRESCRIPTION COSTS, AND OTHER RECURRINGBILLS

WEALTH TRANSFER – ASSETS DESIGNATED FOR YOURHEIRS

HEALTH CARE – ASSETS COVER EXPENSES BEYOND ROUTINE PRESCRIPTION AND DOCTORS’ BILLS, SUCH AS THOSE FOR EMERGENCY AND LONG-TERMCARE

EMERGENCY/OPPORTUNITY FUNDS –IMMEDIATE CASH FOR EMERGENCIES OR FINANCIALOPPORTUNITIE

ACTIVITY 4A

Identify which part of the pie your different expenses would consume.